Your best adjusters shouldn't spend their day chasing incomplete claims.

Catch incomplete and inconsistent property claims before they reach your adjusters.

Incomplete claims waste time. Inconsistent claims waste money.

A missing field costs you a follow-up email.

Wastes timeThe expensive one is the claim that looks finished but doesn't hold together.

That claim doesn't get bounced. It gets assigned, worked, and unwound later, after your adjuster has already spent hours on it.

Wastes moneyAverage property claim, first notice of loss to final payment.

Even in a strong year for the industry.

Reduction in not-in-good-order (NIGO) claims and the rework they cause.

One carrier engagement, after standardizing intake data.

Friction that enters at intake, in the first hours, when a claim arrives that isn't ready to work, compounds through everything downstream. Better information up front is what moves that number. The carrier study behind that 70% also found 60% of identified savings sat in claims leakage, with intake data quality named as a specific driver.2

1 J.D. Power 2026 U.S. Property Claims Satisfaction Study.

2 The Lab Consulting, insurance carrier claims-operations case study.

What a single gap sets off.

Quixas stops the chain at intake.

Before the first adjuster hour is spent.

Two gates, one pass.

Completeness

Is everything your rules require actually there?

Not a generic checklist. Yours.

Consistency

Does the claim agree with itself? Quixas reads the whole package together and checks that:

The stated peril is consistent with the damage described in the narrative and shown in the photos

The loss date falls inside the policy term

The ACORD form, the email, and the attachments tell the same story

Names, addresses, and policy details line up across every document in the package

A field checker catches the first kind of problem. Catching the second takes cross-document reading against rules that encode how your best adjusters judge a file. That is what Quixas runs.

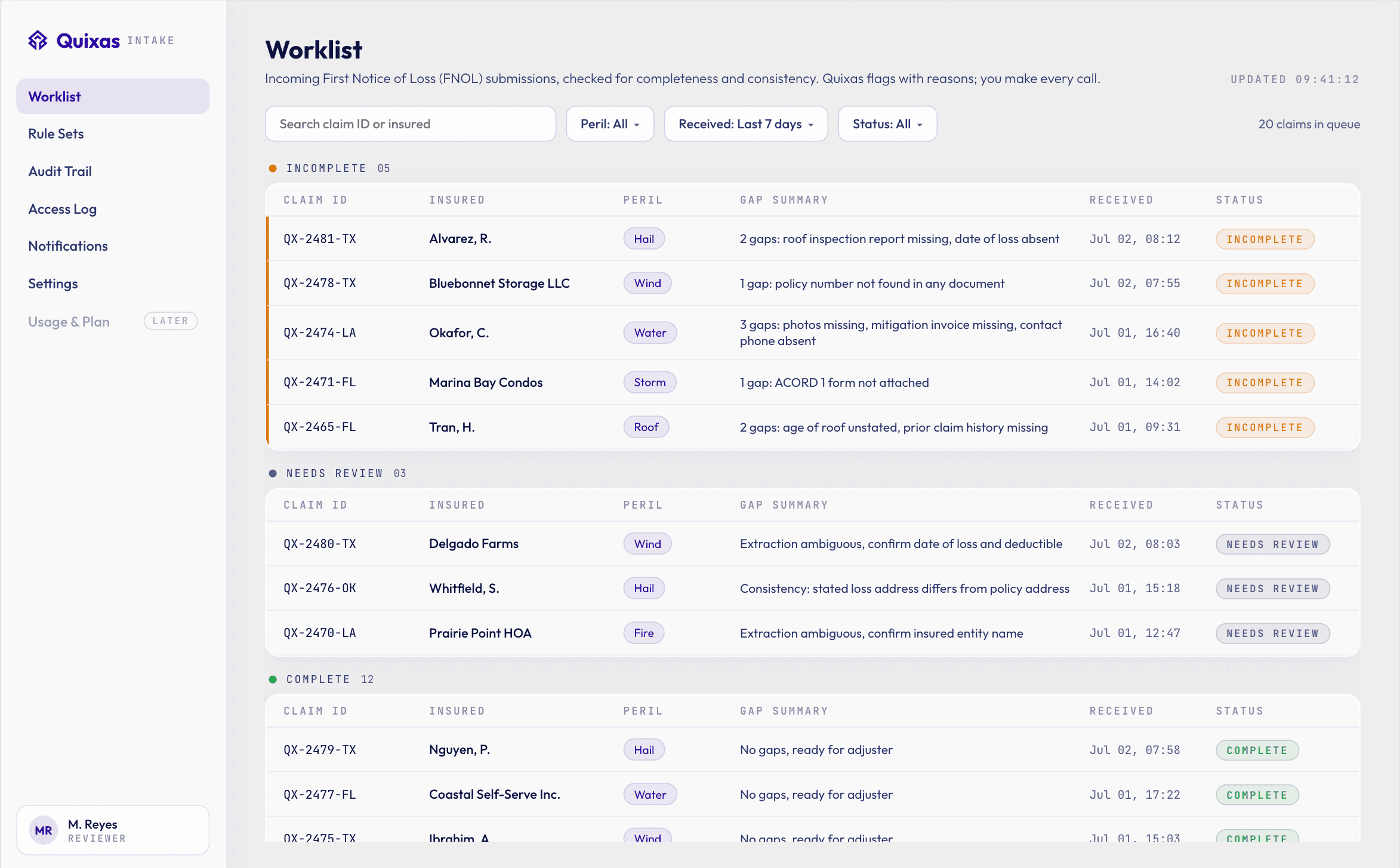

Unstructured inputs in. Checked claims out.

Quixas reads raw inputs from your channels and returns checked, ready-to-work claims, or flags exactly what is missing or what doesn't line up.

Read The Whole Package

A forwarding rule sends the FNOL in. Quixas reads the email, the ACORD form, and the attachments together, as one claim, not as separate files.

Checked Against Your Rulebook

Required fields confirmed, and every document cross-checked against the others. Peril against narrative. Loss date against policy term. Form against email.

Complete, Consistent Claims Routed On

Claims that pass flow straight to the assigned adjuster. Claims that do not come back flagged, with the reason and a drafted follow-up.

Secure property claims ingestion.

Watch it catch a claim that looks fine.

The gate reads each claim, runs the checks, and returns the flags with reasons. This is the queue your team sees: every gap named, before an adjuster opens the file. Open the live simulator to step through a real sample.

Three steps.

It receives the claim

By a forwarding rule from your intake mailbox, or by secure upload.

Checks consistency and completeness

Against rules built around your book. Every document in the package read against the others. Nothing touches your core systems.

Your team makes the call

Complete, consistent claims flow on. Flagged ones come back with the reason and a drafted follow-up. A human decides what happens next.

The checker is easy. The rules are hard.

Any tool can catch a missing field. The real work lives in three places.

Rules per book

What complete and consistent mean for a Florida wind claim versus a Texas hail claim.

Kept current

Across carrier programs and storm seasons, as they change.

Stands up to an audit

Your rulebook holds up when a carrier audits your intake.

That is what we build with your adjusters.

How we build your rulebookFirms that own their FNOL intake.

Run Quixas on last month's FNOLs.

Forward a sample of your historic FNOLs. We build your rulebook from your own claims and your own adjusters' judgment, then show you exactly which claims the gate would have flagged, and why. Including the ones that looked complete but weren't consistent.

It begins with a $2,500 setup and configuration fee. Your first 30-day subscription is waived while you run the pilot. After 30 days, you decide whether to subscribe. Refund terms are in our Refund & Cancellation Policy.